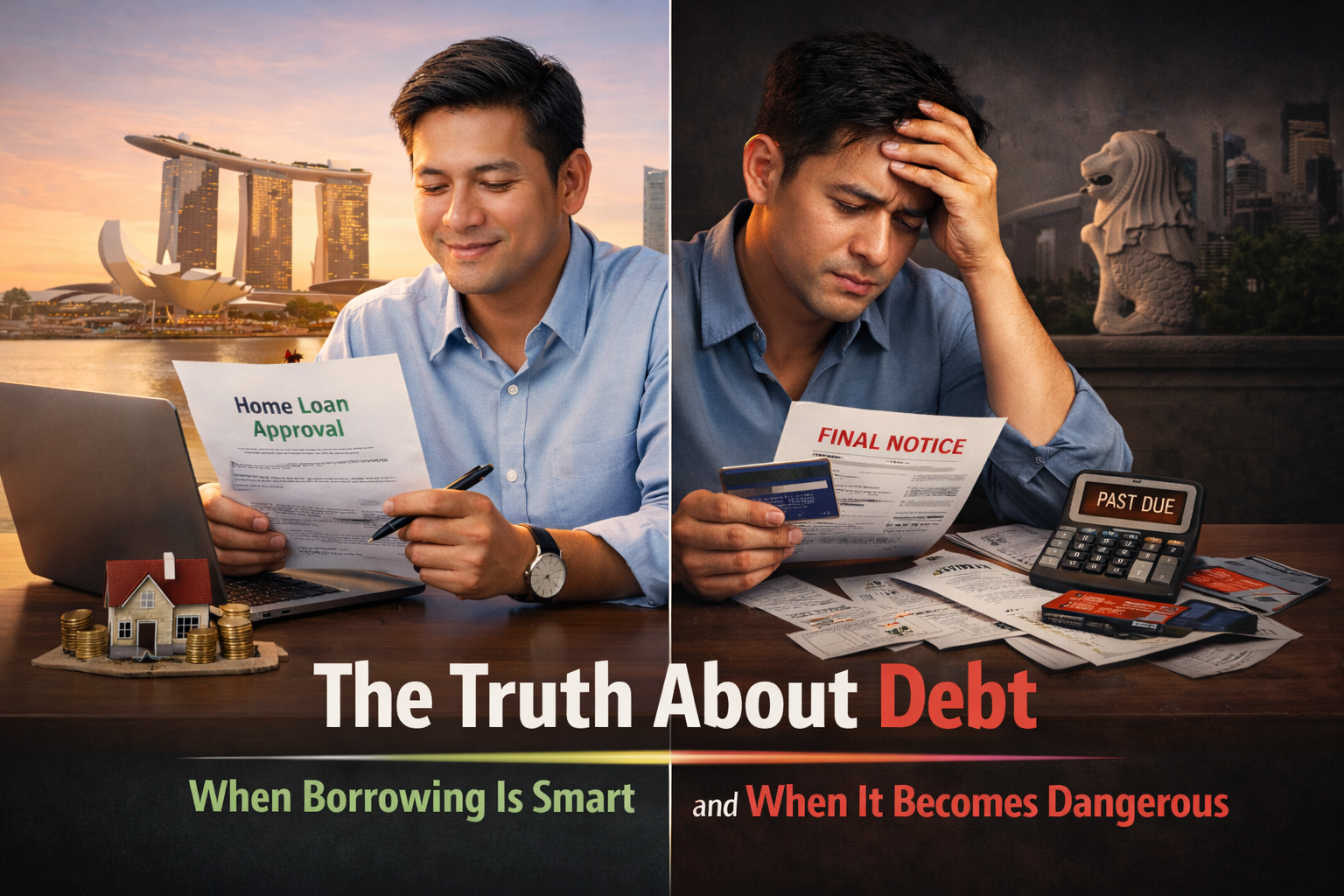

The Truth About Debt

When Borrowing Is Smart and When It Becomes Dangerous

Debt is often viewed negatively, and for understandable reasons. Many people associate debt with financial stress, sleepless nights, and long-term obligations that seem impossible to escape.

However, the truth is that not all debt is bad.

In fact, when used wisely, borrowing can help individuals achieve meaningful goals such as education, home ownership, or business growth. The key lies in understanding the difference between productive debt and destructive debt, and recognising the warning signs before debt begins to spiral out of control.

In this article, we explore when borrowing can be financially beneficial—and when it becomes dangerous.

Understanding the Two Faces of Debt

Debt itself is not the problem. The real issue is how and why the money is borrowed.

Broadly speaking, debt can be divided into two categories:

1. Productive Debt (some might say it as The Good Debt)

2. Destructive Debt (The Bad Debt)

Recognising the difference can make a significant impact on your long-term financial health.

Productive Debt: Borrowing That Builds Your Future

Productive debt refers to borrowing that has the potential to increase your financial stability or earning power over time. In other words, it helps create value.

Examples include:

Education Loans

Education can improve career opportunities and earning potential. When managed responsibly, student loans can be considered an investment in your future.

Home Loans

Property ownership can build long-term equity. While mortgages are significant financial commitments, they allow individuals to gradually build an asset rather than paying rent indefinitely.

Business Loans

Entrepreneurs sometimes use loans to expand a business, invest in equipment, or scale operations. When planned carefully, such borrowing can generate income beyond the cost of the loan.

However, even productive debt requires discipline. Borrowing beyond your means can turn a useful financial tool into a heavy burden.

The guiding question should always be:

“Will this debt improve my financial position in the long run?”

If the answer is uncertain, caution is necessary.

Destructive Debt: Borrowing That Works Against You

Destructive debt occurs when borrowing does not contribute to financial growth, but instead creates long-term financial pressure.

This type of debt is often driven by lifestyle spending or short-term gratification.

Common examples include:

• Excessive credit card spending

• Personal loans for luxury purchases

• Buy-now-pay-later purchases that accumulate quickly

• Borrowing to support a lifestyle beyond one's income

Unlike productive debt, destructive debt typically loses value immediately while the repayment obligation remains.

For example, a luxury gadget bought with borrowed money begins depreciating the moment it is purchased—but the debt continues to grow with interest.

Over time, this can trap individuals in a cycle where new debt is taken just to keep up with existing obligations.

The Hidden Danger: Interest Traps

One of the most underestimated aspects of borrowing is interest accumulation.

Interest is essentially the cost of borrowing money. While it may appear small at first, it can grow significantly over time.

For example, high-interest debt such as credit cards may carry annual interest rates exceeding 20%. When balances are not paid in full each month, interest begins to compound.

This means:

• Interest is charged on the original balance

• Then interest is charged on the accumulated interest

As a result, debt can grow faster than many people realise.

What started as a manageable amount can slowly expand into a much larger financial burden.

This is why many financial advisors emphasise the importance of addressing high-interest debt early before it becomes overwhelming.

Credit Cards: A Powerful Tool or a Financial Trap?

Credit cards are among the most commonly used financial tools today.

When used responsibly, they can provide convenience, rewards, and short-term flexibility.

However, when misused, they are also one of the fastest ways to accumulate expensive debt.

The Minimum Payment Trap

One of the biggest pitfalls is paying only the minimum monthly payment.

While this may temporarily ease cash flow, it significantly extends the repayment period.

For instance, a balance that could be cleared in a few months might take years if only minimum payments are made—while interest continues to accumulate.

The Illusion of Available Credit

Credit cards can create the perception that more money is available than actually exists.

Because payments are deferred, spending may feel less painful than paying with cash.

This psychological effect often leads to overspending without immediate awareness.

Multiple Card Balances

Many individuals carry balances across several cards.

This complicates repayment, increases interest costs, and makes it harder to track total debt.

Without careful monitoring, balances can quietly grow larger each month.

Warning Signs That Debt Is Becoming Dangerous

Debt problems rarely appear overnight. They usually develop gradually.

Some early warning signs include:

• Regularly paying only minimum credit card payments

• Using new credit to repay existing debt

• Feeling anxious about checking financial statements

• Having little or no emergency savings

• Borrowing to cover everyday living expenses

Recognising these signs early can help prevent financial stress from escalating further.

Building Healthy Borrowing Habits

Borrowing responsibly is less about avoiding debt entirely and more about maintaining financial awareness and discipline.

Healthy borrowing habits include:

• Borrowing only for meaningful or productive purposes

• Ensuring repayments comfortably fit within monthly income

• Avoiding high-interest debt whenever possible

• Keeping track of total obligations

• Maintaining an emergency savings buffer

These practices help ensure that debt remains a tool rather than a trap.

When Professional Guidance May Help

Sometimes debt situations become complicated, especially when multiple loans, high interest rates, or unexpected financial setbacks are involved.

Seeking professional guidance can help individuals:

• Understand their current financial position

• Explore practical debt management strategies

• Evaluate options for restructuring repayment obligations

Early advice can often prevent financial challenges from becoming more serious later on.

Final Thoughts

Debt is not inherently good or bad—it depends on how it is used.

When managed wisely, borrowing can support important life goals and financial growth. But when debt accumulates without a clear plan, it can quickly become a source of stress and instability.

The key is awareness.

By understanding the difference between productive debt and destructive debt, being mindful of interest costs, and avoiding common credit card pitfalls, individuals can make more informed financial decisions.

Financial stability is not about avoiding every financial obligation, but about ensuring that each financial decision moves you closer to long-term security rather than further away.

Struggling With Debt? You Are Not Alone.

Many individuals and families face financial stress due to rising living costs, unexpected expenses, or accumulated debt.

At Finesse Advisory, we help individuals understand their financial situation and explore practical solutions for regaining stability.

Our advisors provide guidance on:

• Debt management strategies

• Financial restructuring

• Understanding available repayment options

Reach Out To Us In Confidence.

If you are unsure how to move forward, speaking with a professional can help clarify your options. Reach out to us in confidence by filling up the form below.